By Santiago Hunt

Cover image by Anna Nekrashevich

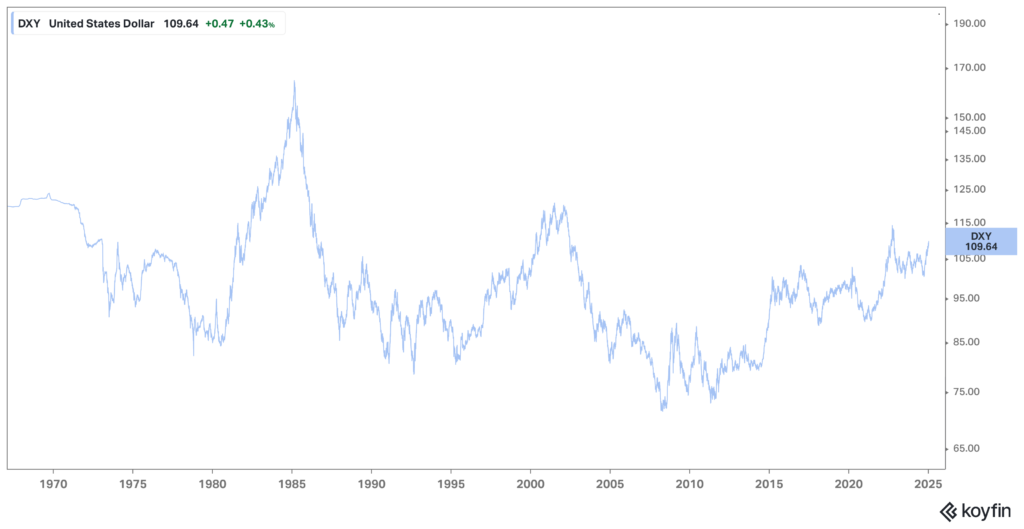

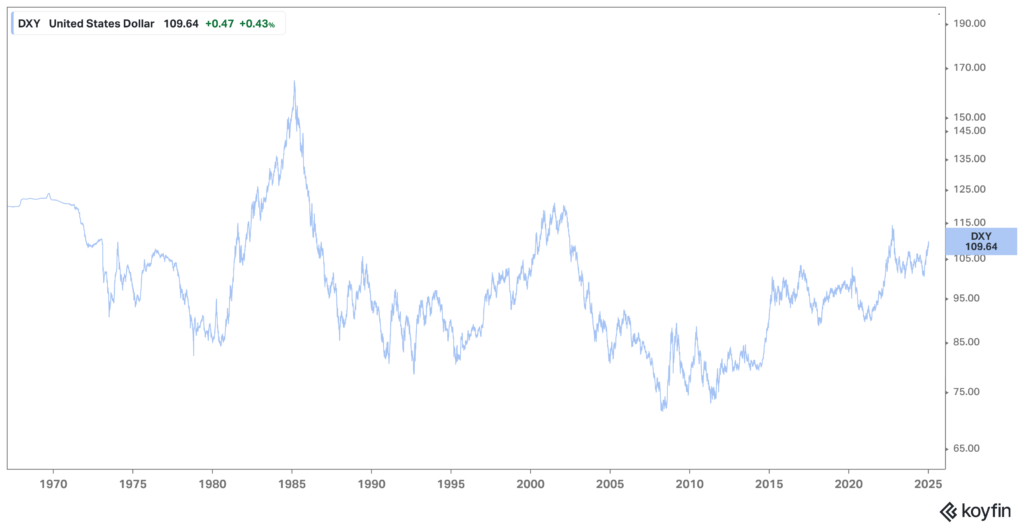

50 years of history fit in just one chart. One single data point. Believe it or not.

The chart in question? The DXY Index. This index measures the strength of the US Dollar relative to a basket of other major currencies. The amount of information compressed into its price evolution is astonishing.

Fifty years is a considerable span of time. To make sense of it all, I’ll break down the narrative based on the major shifts visible in the DXY’s trajectory over time. Now, as with any historical account, this one will inevitably be incomplete and reflect a certain bias. That’s just the way it is.

Prologue (Pre 1975)

In 1971, the United States made the decision to abandon the Bretton Woods system, effectively severing the dollar’s link to gold. This dramatically altered the global financial landscape. America’s allies, accustomed to fixed exchange rates against the USD, were suddenly thrust into a world of “floating” currencies.

Following this change, the US dollar experienced a precipitous decline between 1971 and 1975, shedding approximately 20-25% of its value. This marked an unprecedented shift in the global economy.

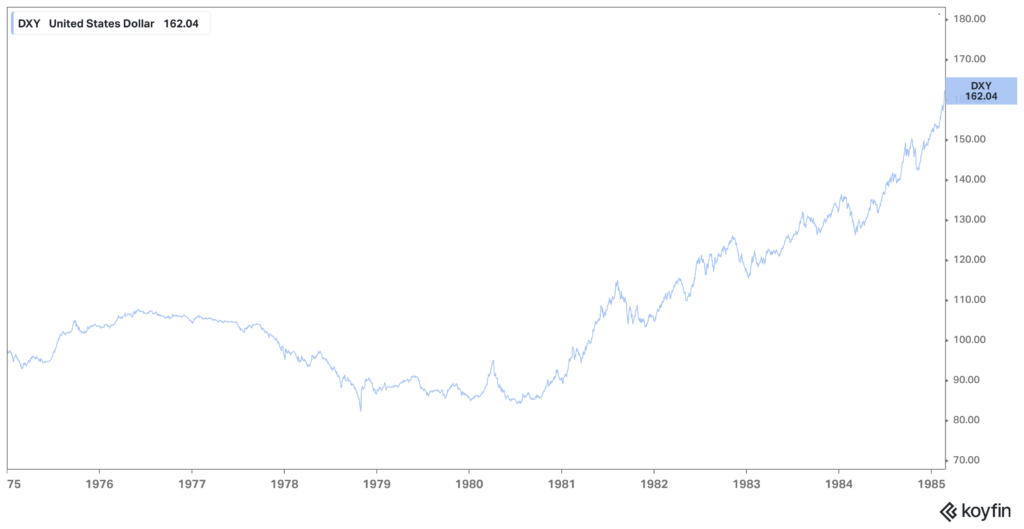

Part 1: 1975-1985: Saving the USD to win the Cold War.

DXY: Drops to ~80 (1979) before surging up to ~160 (1985)

The year is 1975, and the United States finds itself in a precarious position. The Vietnam War, a conflict that exacted a heavy toll on the nation militarily, economically, and culturally, has just ended. Adding to the turmoil, the Watergate scandal has rocked the foundations of American politics.

Meanwhile, European nations are eyeing the US with growing doubt. Their own currencies are appreciating, prompting them to reconsider their position vis-à-vis their American allies. The shadow of the USSR looms large, and doubts are surfacing about America’s ability to maintain global order. The 1973 oil crisis, initially perceived as an isolated event, is now compounded by a second crisis in 1979, causing oil prices to double within a year and sending inflation spiraling out of control.

1979 is a pivotal year. Paul Volcker is appointed Chairman of the Federal Reserve. Volcker is intimately familiar with the intended design of the post-Bretton Woods dollar, and he sees that it’s failing. He’s also worked alongside Henry Kissinger. Legend has it that Kissinger, upon learning of Volcker’s new role, delivered a stark warning: “If the dollar fails, Europe will fall to the USSR.”

The stakes are high. Volcker understands that maintaining the US dollar’s status as the de facto global reserve currency is critical to winning the Cold War. Armed with this conviction, he takes the drastic step of raising interest rates to unprecedented heights. This bold move plunges the US economy into a deep recession, destroying Jimmy Carter’s political legacy. Yet, it achieves its intended purpose: it crushes inflation and saves the dollar.

1981-1985 witness a strong turnaround for the American economy. Under the Reagan administration, growth reignites, and the US dollar solidifies its position as the undisputed currency of global commerce. Reagan’s landslide victory in the 1984 election, one of the most decisive in modern American history, underscores this resurgence. During this period, the DXY index skyrockets from the low 80s to a staggering 150-160 in a mere five years, reflecting the dollar’s newfound strength, culminating in the Plaza Accords in 1985 (a joint G-5 agreement to devalue the USD).

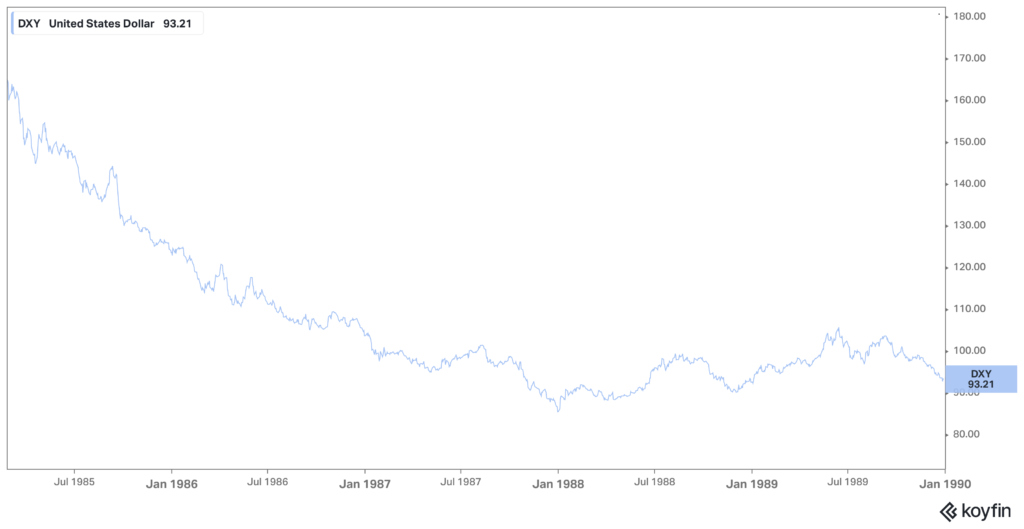

Part 2: 1985-1990: The End of the Cold War

DXY: Drops from ~160 to ~90s (1990)

By the mid-1980s, the tide has turned in favor of the United States. The Cold War is in its waning days. The Soviet Union and its satellite states have been showing signs of strain for multiple years. The US has established itself as the world’s preeminent power. Capitalism has become the dominant global economic model. The back half of the decade sees the ascendancy of American soft power. Companies like Coca-Cola, McDonald’s, and Disney spearhead the expansion of American cultural influence across the world.

Perestroika is led by Gorbachev at first, and later by Yeltsin. The (very messy) transition takes place, ushering an era of opportunity for eastern Europe…but also of suffering. Unfortunately, most people in these countries get exposed to “crony capitalism”, instead of the idealistic westernized version they were promised.

Nevertheless, the Cold War is done. Inflation has been squashed. Rates have fallen. In return, the USD has normalized its value vs. other currencies. What now?

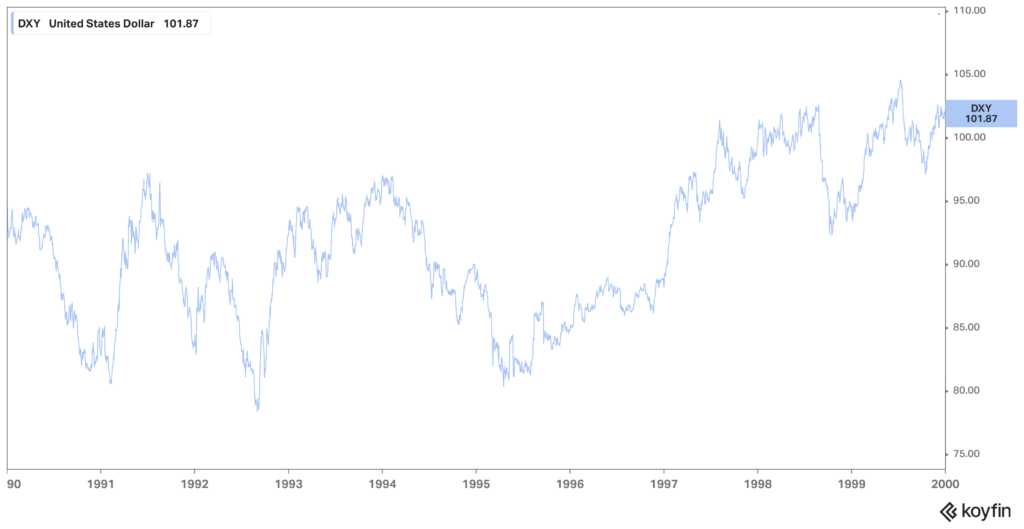

Part 3: 1990-2000: Pax Americana and the dawn of the Digital Age

DXY: Ranges between ~80 and ~100

The 1990s solidify the United States’ position as the world’s sole superpower, introducing an era of Pax Americana. While the decade presents geopolitical and economic turbulence – such as the Gulf War, or the Asian financial crisis – the conclusion of the Cold War frees the US to establish the foundations for the new millennium. The “peace dividend” is born.

This decade marks the birth of the modern world as we know it. The Internet becomes mainstream. Companies like Nvidia, Google, Amazon and Netflix are born. Concurrently, the backhalf of the decade sees an expansion in American productivity. Freeing up resources from War (be it hot or cold) is good for the economy, and the DXY sees a strong rise, going from the ~80s to the ~120s in just 5 years.

Towards the end of the decade the Euro is born (although it will only be fully introduced in 2002). Meanwhile, still under the radar, China has initiated a series of structural reforms where it embraces open (or opener?) markets, under the leadership of Jiang Zemin.

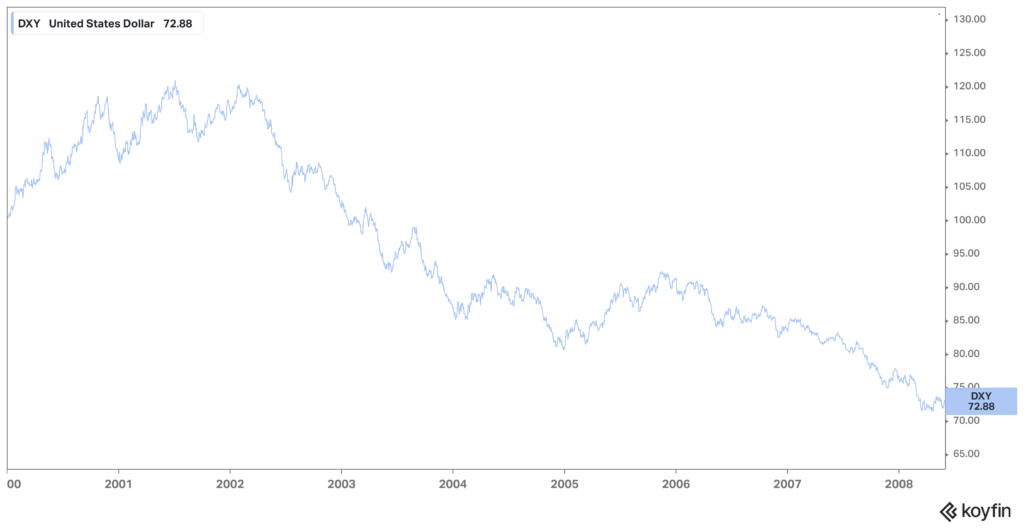

Part 4: 2000-2008: China and the Commodity Supercycle

DXY: Rises up to 120 (’02) then collapses down to ~70 (’08)

The dawn of the 2000s is marked by the bursting of the Dotcom bubble. The ensuing financial crisis, despite a reduction in interest rates, paradoxically reinforce the US dollar’s status as a safe haven, given America’s position as the world’s dominant power. Consequently, the dollar continues its ascent, peaking between late 2001 and early 2002.

However, the most important development of these years is how China’s GDP per capita hits escape velocity when it crosses ~4000usd per capita. China now has something it hasn’t had in over 100 years: a burgeoning middle class. The reforms initiated by Jiang Zemin and continued by Hu Jintao payoff in spades, and China becomes a highly relevant global player, be it politically, economically, or culturally.

The corollary is that China starts to buy lots of things (particularly commodities) from lots of countries. Despite being a major trade partner, the US sees its exports to China lag their fair share. A new rivalry is born.

Because of this dynamic, the USD sees a steep decline. China rises. Europe harbors its golden dream, as it believes (or pretends to believe) it has a unified cultural and economic identity which is strong enough to compete with the US.

These years come to an abrupt close with the GFC. With the USD seeing lows it has never experienced before, all sorts of buying frenzies ensue. Americans (and foreigners) rush to spend their quickly devaluating USD, but they don’t really consider what they’re purchasing in exchange. The housing bubble expands and bursts.

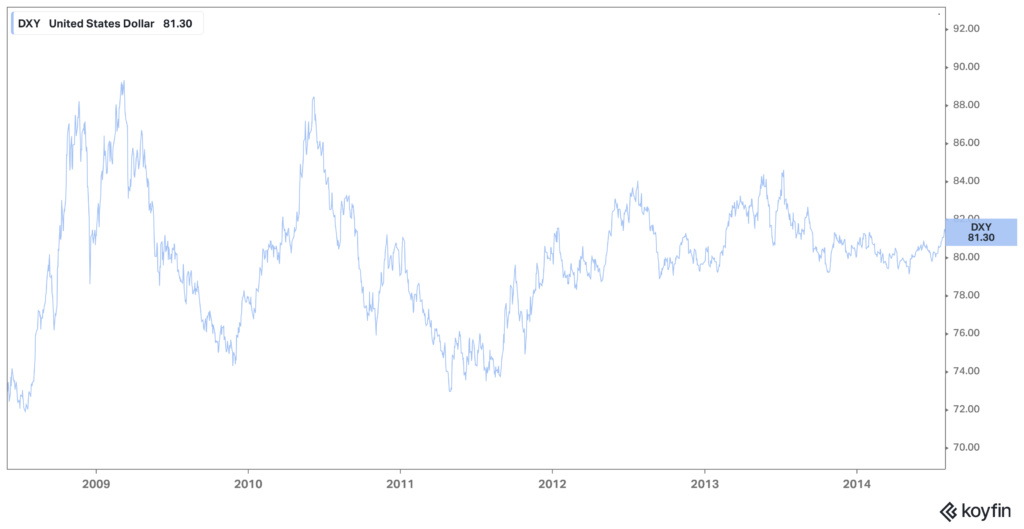

Part 5: 2009-2014: The Rise of Silicon Valley

DXY: Jumps from ~70 to ~90, and later stabilizes near ~80

The 2008 GFC, while not the focus here, establishes a floor for the US dollar. In the following years, the DXY fluctuates within a defined range. This period sees four key developments that reshape the global order.

- European tension: Unable to devalue their currencies, the PIIGS face economic hardship, shattering the illusion of a unified European identity.

- China’s Housing Bubble: China’s efforts to stimulate its domestic economy lead to an unprecedented real estate bubble, particularly visible in its Tier 2 and Tier 3 cities, many of which become literal “ghost towns”.

- US Energy Independence: Shale oil production in the Permian Basin reaches critical mass, transforming the US from a net energy importer to a net exporter.

- Silicon Valley rises: The heavy work that took place during parts 3+4 comes into fruition. The US now houses the biggest value creation engines of the whole planet.

The last bullet is by far the most important one. These companies have a strong compounding edge which allows them to make 1+1=3, printing money in the process. And they’re American, at least for the most part (ex-Taiwan semis).

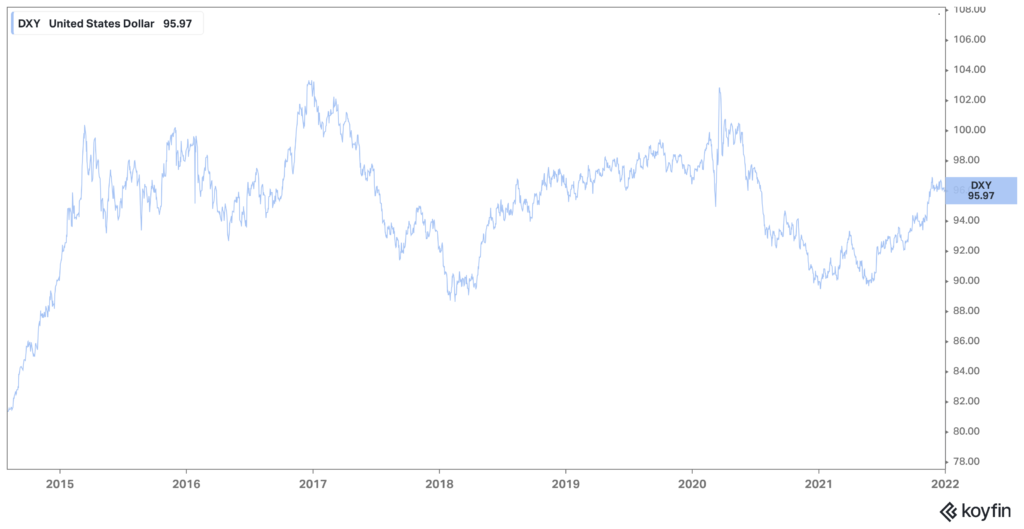

Part 6: 2014-2021: Pax Silica powered by shale oil

DXY: Shoots up to 100 (2015) – later ranges between 90/100

The shale revolution fundamentally reshapes the global energy landscape. With the US now a major oil producer, OPEC’s influence is reduced. Oil prices plummet from over $100 to the high $20s before stabilizing in the 30-40s.

This newfound energy independence, combined with Silicon Valley’s continued dominance, fuels a strengthening US dollar. The DXY surges. Despite some volatility, the dollar achieves a unique stability at higher prices, a phenomenon not seen since before the end of Bretton Woods. The US increasingly diverges from the economic paths of Europe and Japan.

This period comes to an end with COVID and the inflation surge that followed. Leading us to today…

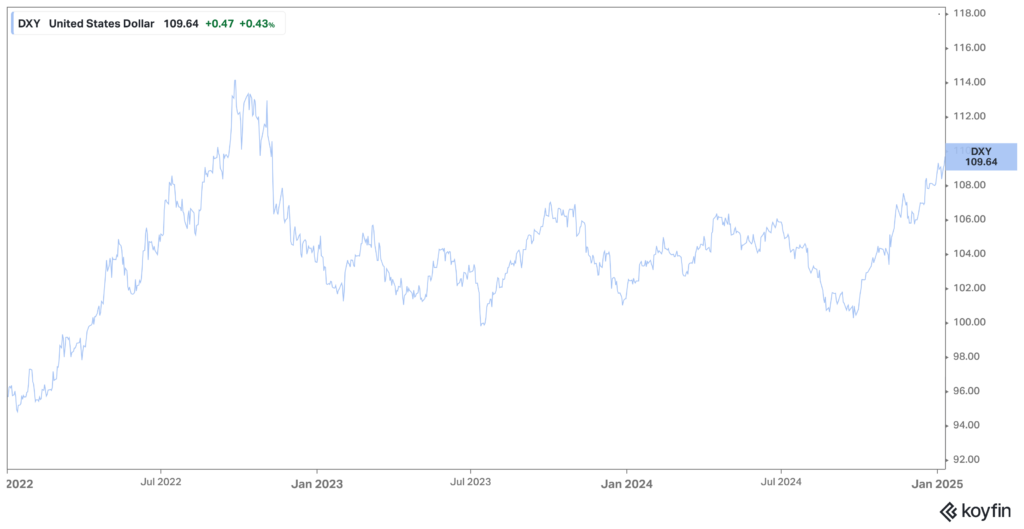

Part 7: 2022+: The AI era?

DXY: From 90 to 115 (2022) – then ranges between 100-110

Following the COVID-19 pandemic, a confluence of factors—excess liquidity, tight labor markets, and disruptions in energy supply chains—fueled a global resurgence of inflation. As this inflationary pressure gradually subsides, the USD has now firmly established itself above the ~100 mark (currently at 109).

This higher level reflects the widening gap between the US and the rest of the world in terms of economic dynamism and technological advancement. While it faces competition in certain sectors (e.g., Chinese automobiles, electronics, and renewable energy equipment), the overall US economy stands at a formidable juncture.

The rise of AI has the potential to further widen this gap, leading to an even stronger USD. While the future remains uncertain, here are some provocative thoughts to consider (some might contradict others):

- US Market Dominance: The US stock market becomes the de facto Western/global market.

- Tech Giants’ Ascendancy: The “Magnificent Seven” tech giants consolidate their power, asserting themselves as the most influential force globally. War breaks out between them.

- Constraints on Commodities: A “commodity supercycle” will not happen with the DXY above 100, potentially disappointing emerging markets hoping for a repeat of the 2000s.

- Chinese Yuan Devaluation: Despite efforts to maintain stability, China eventually devalues the yuan (USDCNY above 8) within the next 5-10 years.

- AI-Driven Unemployment: The rapid advancement of AI leads to unemployment surges in developed markets, fueling social unrest, particularly in the EU.

- Asian Currency Vulnerability: Demographic challenges in some Asian countries might trigger currency and societal collapses (e.g., South Korea).

Will we see the DXY fall below 100? It can definitely happen under a Trump administration – for a while. However, unlike the 1985 Plaza Accords, no other countries currently have the capacity to absorb a significant revaluation of their currencies. Ultimately, for a weaker USD to occur in the long run, deep and structural power shifts need to occur.