By Santiago Hunt

(Cover picture by Lamar Belina)

Most of us identify ourselves to some extent with contrarian thinkers. We like to think we are somewhat contrarians as well. After all, there’s a reason we root for the misfits, the lone wolves and the Cinderella stories in movies.

Here’s the thing though: It’s HARD being a contrarian. You must have an idea or worldview that clashes with what the majority believes. And having an “unpopular” idea is not enough: Being a contrarian requires staking this idea in public. In other words, having “skin in the game”. Be it via an investment or a manifestation of sorts, being a contrarian means being exposed. You must open yourself to attack, be it moral, economic, or intellectual.

What’s tougher than being a contrarian thinker? Being one without becoming a zealot believer. Good contrarians trace a line which invalidates their views and monitor it closely. Absent this line, there’s no difference between them and zealots. “Flat-earthers” could be excellent examples of contrarian thought, except for the fact that seemingly nothing will falsify their views.

Flat earthers are rare, but the investing world is full of another category of pseudo-contrarians: “perma-doomsayers”. Pundits who are always prognosticating the collapse of the financial system in one form or another. Eventually, they end up being partially right: Corrections are a given (we are in a strong one right now), and they will display their victory parades accordingly. The thing is, they have predicted 9 out of the 2 last crisis. When assessing these commentators and their views, it’s critical to see if they’re time/space constrained, or open and vague. If the latter, they don’t fit as true contrarians either.

If being a contrarian is tough, why is it worth it? Many reasons. It trains critical thinking. It dampens mob reactions and forces us to use first principles. It is unscalable, so it forces us to pick the battles in which we’re willing to consider it a viable path. Ultimately, it can result in great value, be it monetary or intangible.

In line with this, I will present 4 contrarian views I have, because being a contrarian thinker requires exposing your own views to criticism and rebuttal. I hope you find them interesting.

1) Solar and Wind energy are mostly hype

Contrarian view: The IEA (International Energy Agency) predicts that wind & solar will account for 20% (US/ChinaLatAm) and 30% (EU) of total energy generation in the year 2026. My view is that this is an extrapolation of the growth curve of the past decade, and therefore critically wrong.

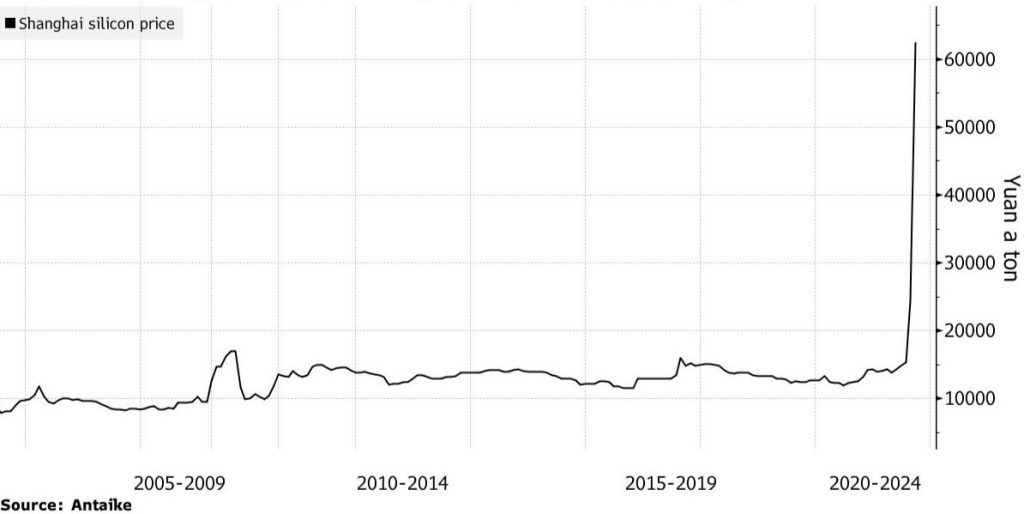

Why? There’s a mix of reasons. Firstly, costs. Wind and solar cost has dropped strongly in the 2010s, but few realize that most has to do with drops in traditional energy costs during that period. Take the example of coal. Carbon is a critical input for polysilicon, which is a key component of solar panels. What happened the prices of polysilicon in the end of 2021 when coal’s price went up?

Inputs for solar panels, batteries and wind turbines track traditional energy costs. And with the jump we’ve seen in 2021-2022ytd, and no signs of relief in sight, the cost drop outlook will not be the same than what we saw in the past 10 years.

Additionally, there’s a deeper problem which is linked to energetic efficiency. Energy must be spent to produce energy. An elegant way of calculating this is using EROEI (Energy Return on Energy Invested). EROEI measures how much energy is required to generate a useable unit of power. According to Goehring and Rozencwajg, both oil and gas have EROEIs of 30:1 (30 units of energy generated per unit spent to produce them). What’s wind & solar’s EROEI? Adjusting per intermittency and redundancy…under 4:1. That means that wind & solar are 7x more inefficient than traditional O&G sources.

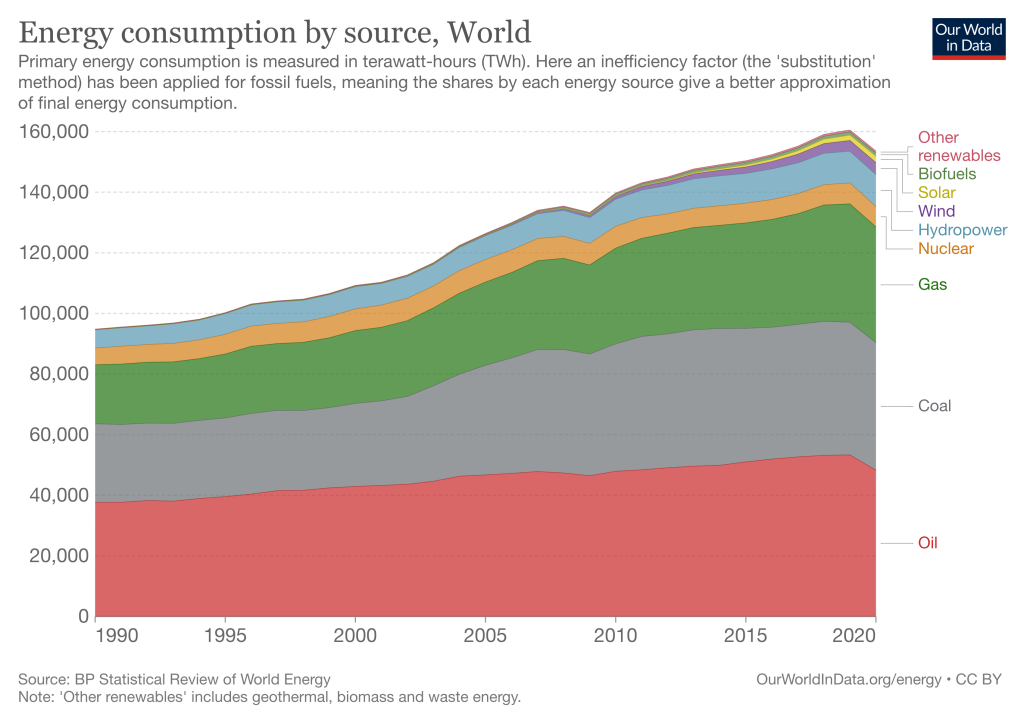

You might be thinking that nevertheless, we must continue our energy transition given GHG emissions and their climate change impact. Here’s the issue though: Our so-called transition is a fairytale. In the past 30 years, we have not reduced traditional fossil fuel usage at all. And these where years with i) heavy cost reduction windfall for renewables ii) heavy governmental subsidies.

Perhaps you might believe that technology improvements will solve these challenges. The issue with this goes back to the basics of physics. Wind and solar are high entropy energy sources: they are more fickle/volatile. Intermittent, variable, unstable per se. The degree of scientific breakthroughs required to make up for a 7X efficiency gap is huge…and will likely not live up to expectations.

Does this mean clean energy is doomed? No. Gas is a cleaner alternative to coal/oil which is not being fully exploited today. Furthermore, there’s an incredible renewable energy source with an EROEI estimated to be 100:1…Nuclear. The barriers nuclear faces are long timelines and cultural misunderstandings which we need to solve…ASAP.

What could prove this view wrong? Sustained drop in wind & solar generation costs coupled with reduction in wind & solar subsidies (current subsidies are unsustainable).

Degree of confidence: VERY HIGH

2) The 21st century will NOT be the “China century”

Contrarian view: Unlike the consensus view, China will not become THE dominant empire of the 21st century.

Why? 2 main reasons. One is energetic. But the main one is demographic.

The first reason has to do with the fact that China is a net energy importer. There’s an anecdote on why the Allies managed to win WWII, despite the fact the Germans had better troops, training, weaponry design and tactics. Simply put, the US had 30 better barrels of oil for each barrel Germany had.

The anecdote is a clumsy oversimplification of WWII, but it highlights the key role energy plays in our world. And China is a net energy importer. Ie. Every year, 15-20% of its energy consumption is imported (source: WorldBank). While they’re working to address this by ramping up nuclear, the Chinese are nevertheless behind the curve.

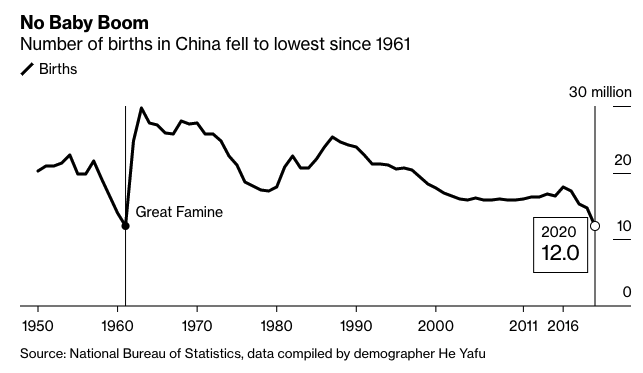

It might take 10-20 years, but the Chinese should make up for it, right? The bigger problem: By that time, China will be facing a dramatic demographic crunch. Years of the “1-child policy” have led to a demographic crisis. 2020 was the year with the lowest number of births in China since the Great Famine (and per capita numbers are even worse).

The CCP is intent on averting a “demographics are destiny” future. “Three child policy” (三孩政策) is now in place, and authorities are keen on enforcing it. This had led to a crackdown against LGBT minorities, restrictions against videogames and a very vocal message behind “family values” from Xi Jinping and the CCP. All of this is driven by China’s biggest challenge: Their urgent need to drive higher birth rates.

Unless China finds a way to turn the demographic tide, they will become a Japan 2.0 in the next 15 years but at a lower GDP per capita. This in turn will lead to increased social unrest. Many things have been tolerated by the Chinese people given their economic growth in the past 30 years. If this stalls, expect a domino effect.

One important point: China will obviously be a highly relevant global player. My point is that they will not become THE relevant world superpower. We will continue moving towards a multipolar world with a dwindling but still relevant USA + a growing India (the dark horse in the 21st century race).

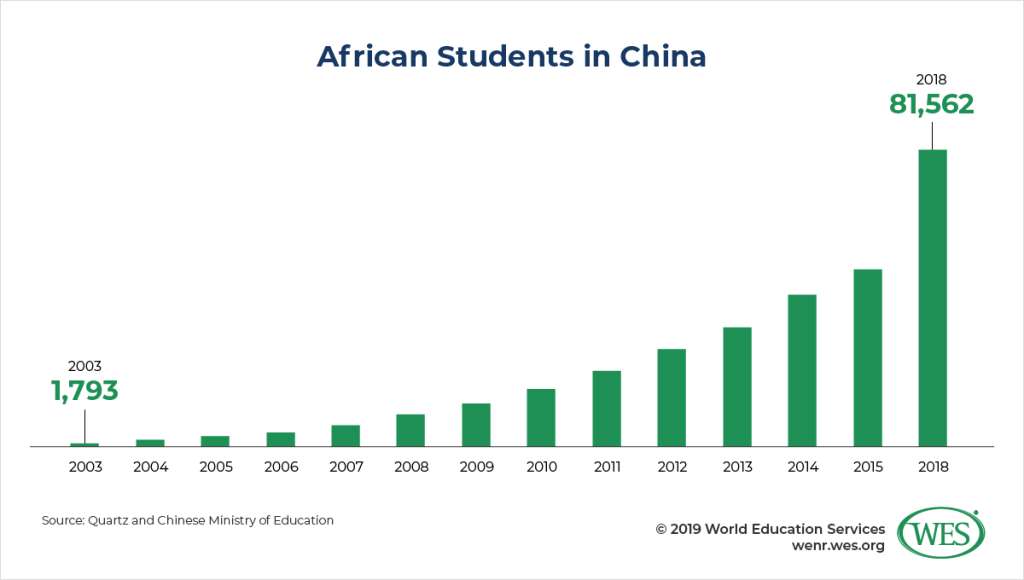

What could prove this view wrong? Either a steep step up in economic growth in the short term (unlikely) or a steeper change in births (even more unlikely). Absent these, massive immigration is the only card China has left. Keep an open eye on Chinese/African ties as a potential human capital basin (See below).

Contrarian view degree of confidence: HIGH

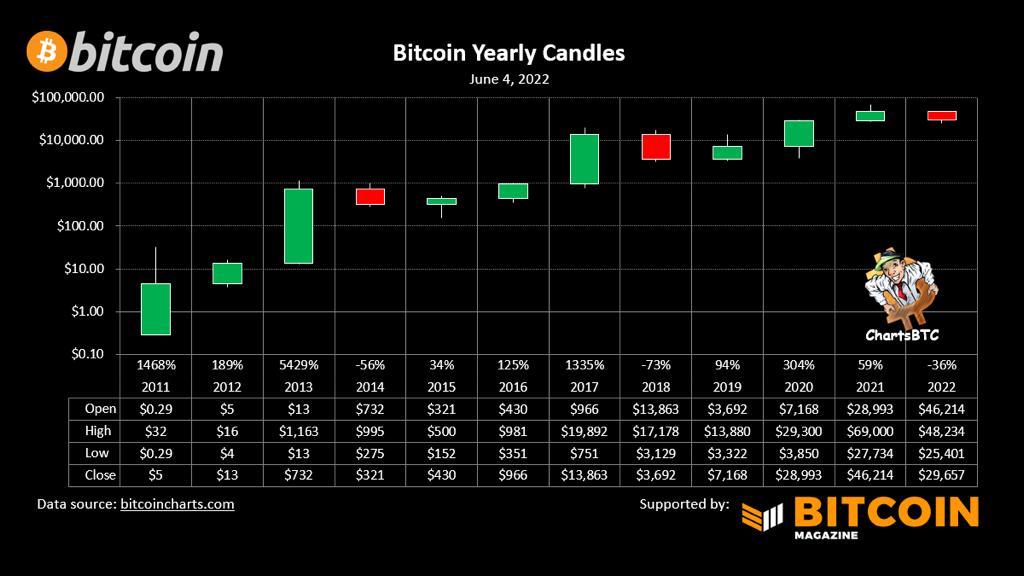

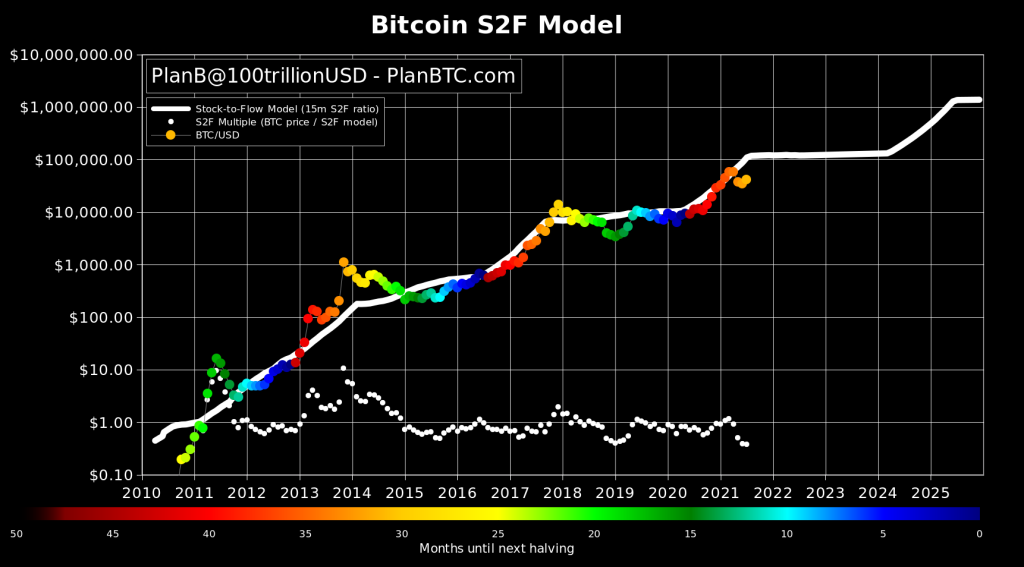

3) Bitcoin will not go under 20K (at least in 2022)*

Contrarian view: Bitcoin will not consistently go under its 200W SMA – at least in 2022. *: I use 20K for simplicity but the 200W SMA is the number to watch.

Why? When I drafted this (a week ago), my contrarian view was that people were too optimistic regarding Bitcoin/crypto prices. The last 72hs have made that view stale. It was only last week that this chart was making the rounds in Twitter, with a good degree of “hopium” attached.

Consensus seemed to be in the lines of “3 green candles, one red candle” coupled with “new bull run after crypto winter”. I’m sure people also remember the S2F “model” (if you can call it that).

Now, the tables have turned violently. At the time of writing, Bitcoin has dropped ~20% in 24hs. People are claiming that it will do a COVID roundtrip and will go back to 10K. Which makes sense, given Bitcoin should be understood as a liquidity vacuum cleaner. Tightening kills Bitcoin price, and the “inflation hedge” case has been proven wrong.

Nevertheless, the 200W SMA is a powerful force that I believe people are overlooking. And last week’s inflation news is not THAT bad to justify breaking it. The odds are well against this claim: it’s likely the S&P will continue to fall, adding negative pressure. And there’s no evidence that the Fed will pause in the short term. But that’s the beauty of contrarian views – if they don’t make you uncomfortable, are they really contrarian?

Some disclaimers: I don’t own Bitcoin. I do believe there might be some downside 200W bursts, which will be short lived. If this view is wrong, it’ll be VERY wrong. I’m not particularly bullish BTC either. ATH, 100K and the likes seem incredibly unlikely unless the FED throws the towel on tightening (which might happen later in the decade). And most important of all, probabilistic thinking >> deterministic thinking. This is not financial advice.

What could prove this view wrong? The FED doing 75-100bps increases at any point in 2022.

Contrarian view degree of confidence: MEDIUM (Crypto winters are brutal)

4) England will win the 2022 World Cup

Contrarian view: The title says it all!

Why? This is as contrarian as you can get. Despite betting markets putting ENG as #3-#5 favorite…who honestly believes that England, a team which has consistently disappointed, has any real chances? Probably no one.

The two consistent favorites according to betting markets are FRA and BR. The FRA picture is simple: Name by name, the best team in the world. However, it’s almost impossible to be back-to-back champions. Furthermore, since 1998, past champions have greatly underperformed vs expectations as a norm (we’ve now seen 3 WCs in a row where the past champs can’t make it past the group stage). The stories here are similar: It’s hard to prune and renovate the champion squad, which leads to a team that originally was at prime age 4 years ago having to replay 4 years later, with less stamina and fuller (figurative) bellies. FRA has done a better job than ITA, ESP and GER renovating their team. But repeating 2018 will be a high bar.

BRA is a riddle. They are the other top team out there. However, their collective performance hasn’t been able to fully unlock their individual talent. In Brazil’s case, the sum has been less than the parts. Additionally, BRA hasn’t been able to fully purge the psychological weight that 2014 WC has meant for them.

Which leaves us with the second-tier candidates. ESP and GER are the European counterparts of the Brazilian situation: great individual line ups, but teams that haven’t been able to fully coalesce. ARG on the other hand shows incredible collective strength. The key issue in ARG’s case is “key man risk”. They depend on 3 players: Lionel Messi (obviously), “Cuti” Romero and Lautaro Martinez. If they happen to be injured, in low form or disabled by their opponents, the whole team will feel it given lack of replacements. Finally, NED, BEL and POR cover the remaining top spots in the betting charts. Of these 3, NED has the strongest side, and might cause rivals a lot of pain, but are unlikely to win the WC given their lack of world class forwards.

Which leaves us with ENG. The English, who had the youngest squad in 2018, will hit 2022 at prime age. They’ve shown steady progression since the WC and Euro. They’ve tasted defeat and have evolved due to it. As a collective, they have one of the best defensive sides of the WC, as well as one of the best benches out there. A well-balanced side, that faces a healthy mix of excitement and skepticism. To top this, Southgate is one of the best managers at a national level and will be entering his sixth year behind the English squad.

What could prove this view wrong? ENG fumbling due to pressure.

Contrarian view degree of confidence: LOW – This is soccer, and we’re talking about England after all:)