By Santiago Hunt

On Feb 3rd 2022, Facebook’s stock saw a 27% decrease in one day. This was the biggest % drop for the stock in its history, marking a 250B (!) loss in 24hs.

What happened? A fall in DAUs, TikTok competition…but the chief negative driver was Apple’s ATT (App Tracking Transparency) move hitting Facebook/Meta in full force. What is ATT? More on this below, but the one liner is that Apple has severely reduced tracking activity across apps, which has in turn hurt Meta’s targeting capability.

What’s more important though, is that Feb 3rd marked the shift into a new era of advertising: the Binary Paradigm. How did we get here, and what will it mean for the future? Brief history recap:

Traditional Advertising: Interruption Paradigm (1950s-2007)

For over 50 years, advertising operated under the “Interruption Paradigm”. What was the “Interruption Paradigm”? Due to limited segmentation capabilities, advertisers had little grasp of their ROI. “If only I knew which half of my advertising budget works…” showcases this era’s challenges.

If you can’t properly segment, you need to fish in the biggest pool possible and hope for the best. To do that, you need people’s attention. The more attention, the higher your chances of successfully landing your message. The best strategy? Interruption. Big, resounding ideas that lived primarily on TV.

This was the golden age of “creative”. Because attention was scarce, you had to be bold and different. And because our brains react faster and stronger to emotional stimuli, many messages weren’t confined to plain old rational stories. Instead, there was permission to break boundaries. To be creative.

Probably, the Epitome of this era was Cadbury’s Gorilla ad (2007), which featured 90” of a gorilla playing the drums…in the hopes of driving chocolate sales. (By the way, the ad is brilliant. But it’s also the tombstone of an era).

Modern ADV – Age I: The Conversation Paradigm (2007-2013)

Although Internet was already a thing for ~15 years, it is only around 2007 that “Modern Advertising” comes to be. In a Modern Advertising world, people can now “talk back” at scale thanks to Web2 aka Social Media (In Web1, scale was the missing piece). Suddenly, brands see that audiences are no longer mute. Time to change tactics. No more one-way street messaging. The “Conversation Paradigm” is born.

A new player surfaces: the “Community Manager”. These community managers, unlike today’s automatic bots/software, were real people. Responsible for wide ranging conversations on behalf of brands. Which led to multiple questions: How do we engage with real people? What’s our tone of voice? What do we say? What do we not say?

At this time, Facebook is keen on selling brands a framework called CEII, which stands for something in the lines of Connect – Engage – Interest – Influence. Account executives try to convince advertisers about the importance of “Fans” (remember Fans?), even though it is unclear how to monetize these relationships (for both advertisers and FB).

Meanwhile, Google launches its now failed social network, G+. A good product, with some very avant garde insights, such as the possibility to tailor your online persona based on the audience. Same as how you would behave offline. But network effects are cruel. Google never finds a reason good enough to get people to switch. Turns out inertia is a powerful force!

Twitter/Instagram/Snapchat/Pinterest are launched (many failed social networks as well). Meanwhile in China, social media forks the road and takes a wildly different path than in the West (worth another post in itself).

Many marketers realize something: What happens if your brand is not worth having a conversation? Two subproducts of the “Conversation Paradigm” are born: Purpose-led & Content-led advertising. The former is an attempt at creating deeper meaning for brands. The latter is about making them interesting.

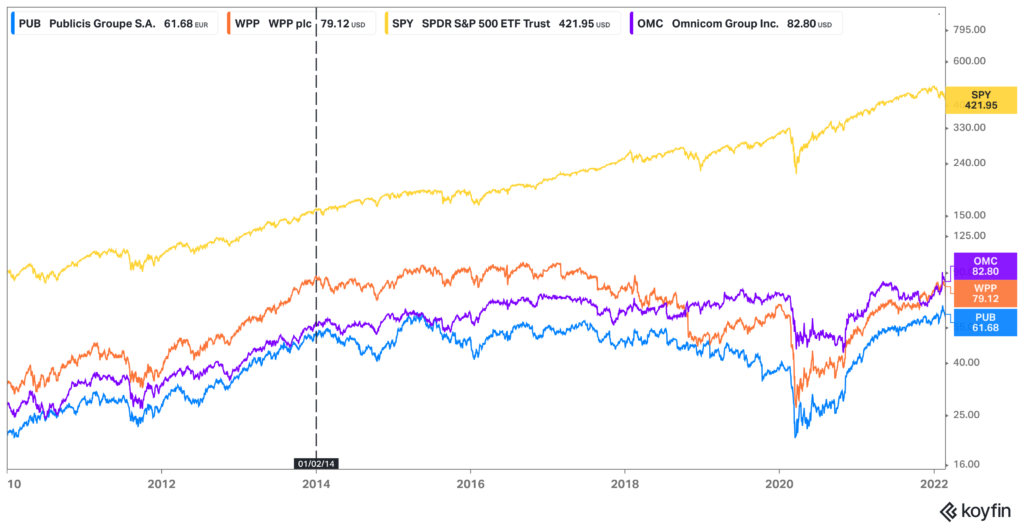

Some brands figure out that it’s hard to do conversations without being fake or irrelevant. Better to hijack existing ones —> Influencers are born. The end of this period marks the peak of ad agencies. Agency stock prices plateau in 2013/2014. Since Jan 2014, Omnicom’s returns are less than 25% of the S&P’s, Publicis’ are only 6% vs. S&P, and WPP’s are directly negative!

Modern ADV – Age II: The Direct Response Paradigm (2013-2021)

Around 2012, FB fully acknowledges the power of smartphones and how the iPhone is truly a game changer. Full pivot towards a mobile advertising model. The acquisition of both IG (2012) and Whatsapp (2014) are a push to increase its “app footprint” on the phone screen. In parallel, Google drops G+, doubles down on Search, YouTube and the Android ecosystem.

Advertisers are now handed the most powerful tools they’ve ever had in terms of reach and segmentation. Already available in search, the flow from ad to conversion that FB/YT offer is frictionless and mesmerizing. Couple of clicks and you’re in. Remember “I wish I knew what half of my adv budget works?”. Turns out now you have an answer.

For those who could execute on this new reality, it is 10x better than conversations around purpose and content. “Marketing as art” dies. Marketing becomes a science (some brands will retain a mix of art and science, but those that don’t embrace science at all suffer a world of pain). Enter the “Direct Response paradigm”.

Smaller companies are the first to embrace the change. Big ticket advertisers such as CPG are trapped by their lack of vision, prisoners of outdated ROI models. The slow pickup makes ROI of FB/GOOG adv crazy good and DTC and especially “Install App” direct response marketing flourish. The most obvious example here are mobile videogames which boom during these years. A less obvious but highly significant winner is Fintech, a clear beneficiary of this new paradigm.

Eventually everyone realizes that, provided segmentation and conversion tracking capabilities, you can understand what consumers need and like. Turns out that if I know what you’re looking for (search) or what you’ll react to (FB), a 1080×1920 ad or 2 lines of well-crafted copy will do. No need to spend 1M in ad production to catch your attention if I know what will make you click.

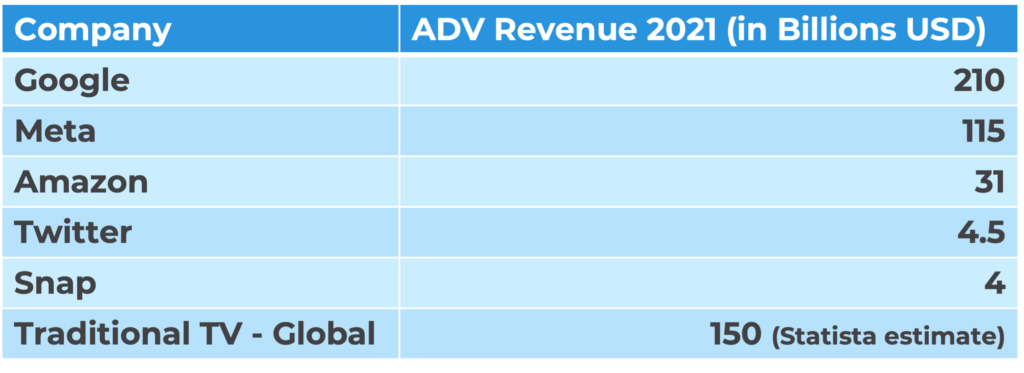

Big ticket companies build in-house ad development capabilities and ad agencies feel the pain. How hard can it be to produce a bunch of banners/text blurbs for keyword search? GOOG/FB respond by ramping up the price of adv. They’re the true value-adders in the equation of customer acquisition, and they start charging for it accordingly now that they have everybody on board. Some competing players start to gain traction in the advertising ecosystem. Amazon (31B in Adv Revenue in 2021) and TikTok are the bigger ones.

The Epitome of this era:

The End of the Second Age

It happened when Apple announced that it was implementing ATT.

What’s ATT? A new set of policies designed to “protect” (note the inverted commas) user privacy. Rolled out with iOS14 starting end 2020. Ben Thompson has greatly documented the specifics of ATT in Stratechery so do check it out for more information.

Why is it meaningful? It maims FB segmenting capabilities via two mechanisms:

- FB used to track not only user activity in its family of apps (which it still does) but the activity in other apps as well via IDFA (Identifier for Advertisers). As of iOS 14, people are now asked upfront if they wish to limit this tracking (most say yes).

- ATT bans FB and other apps from recollecting eComm behavioural data. This is a topic of much speculation as there are multiple gray zones, but for now it’s fair to say that it has impacted FB’s data gathering.

Implications? FB and to a lesser extent Youtube are hurt. The biggest pain though lies with eComm / “Install App” brands, which found in Q3/Q4 that their CAC went up 3-5x or more. Shopify, for whom DTC brands are its lifeblood, has lost 60%+ of its market cap since Nov21, in great part because of this.

Modern ADV – Age III (2021-???)

As we speak, the third age is kicking off. Consider the current statu quo:

Google: In strong shape. It commands search, which is the form of advertising which has pre-existing intent best embedded into it – making it the one where advertisers are most willing to spend. Nevertheless, YT is hurt somewhat by ATT.

Meta: Deeply wounded. But Meta still has 2.8B DAUs, and no direct competitor is near that critical mass. It will likely find ways to navigate this new setting, such as enhancing its in-app shopping capabilities (Whatsapp already showing some of this). However, unless the playing field moves away from phones, Meta is a hostage. This explains why Zuckerberg is obsessed with the Metaverse. It’s his one shot at changing (and controlling?) what today is owned by Apple and Google (iOS/Android).

Apple: Will Apple aim to leverage its data advantage in advertising? Unlikely but not impossible. Apple has tried this in the past (and failed). And Apple is first and foremost about its best-in-class UX. Advertising is a necessary evil, but one that doesn’t go in hand with best-in-class UX. Nevertheless, a few years ago consensus was “Apple is about hardware”, and today it has become a service company enabled by proprietary hardware. A shift to include advertising in its stack cannot be ruled out.

Amazon: Big winner. Lots of DTC advertising dollars will flow into retail, and Amazon is ultimately a retailer in many cases. (Also, big opportunity for Sea Limited and MercadoLibre provided they get the incentive system right).

Traditional TV: While there might be some short-term reshuffling that favors TV networks, it’s a loser’s game in the long run (well below 2010s highs and negative growth estimated).

What about the other “Usual Suspects”?

TikTok: Big short term winner. Further down the road, it all depends on how geopolitics line up.

Twitter: For the first time in forever, Twitter seems to be moving towards more focused and aggressive monetization. There’s a big prize if they do it right. But the risk of breaking the platform in the process is very real.

Snap: Snap has an economics problem. Consider how it makes 7.4USD in Gross Profit per DAU vs 41USD in Gross Profit per DAU for Facebook. Until it solves this, it will not command comparable traction.

And what about the “Unusual Suspects”? (As @modestproposal1 likes to point out, in a long enough timeline, everyone sells ads)

Netflix I believe will trial some form of non-traditional advertising product in the next 5Y. Uber has a fast growing ad platform which already has a 225M run rate. Unity/Epic have a massive opportunity in the space. Videogame integration is a more niche opportunity, but it still poses an interesting option for Microsoft, Roblox and Garena (Sea Limited).

Finally, there’s the “Forgotten Suspects”: Traditional Retail.

In the last few years, as digital CAC went up many brands figured out that the future was omnichannel rather than 100% digital. Today, we find those traditional retailers that were able to adapt to the eComm brave new world in better shape than expected. WalMart, Target, CVS, Boots, Home Depot are some examples of players ready to compete. They will have a strong gravity pull for some of the orphan ADV spend created by this new paradigm.

What will the 3rd Age be about? The Binary Paradigm

A new era in advertising is here: the “Binary Paradigm”. In the Binary Paradigm, seemingly paradoxical realities will coexist. On one hand, we will see “Hyper fragmentation” and “Organic acquisition” forces.

Hyper fragmentation not only of audiences (which exists today), but also of mediums. The beauty of social media is that you can target different groups in the same medium, hence you can expect same type of attention span, engagement, behaviour etc. In this new paradigm, there will be greater need to fragment messages, given advertisers will need multiple channels to make up for Meta. In a weird way, it’s kind of a 2.0 take on 360° Advertising.

Organic acquisition is a theme already present in the past years given rising digital CACs. The flip side of organic acquisition is the need for sharp positioning, which is hard to achieve whilst scaling. We might see an exit/reduction in VC/PE spend in the DTC space, as investors figure out most brands had little to no real organic traction.

At the same time, it wouldn’t be surprising to see more concentration. If Amazon is the Empire and Shopify is arming the Rebels, things sure look bleak for the “good guys”. This Twitter thread from the founder of Native (acquired by P&G) provides good context:

Concentration amongst incumbents will likely be the norm across multiple businesses. Expect the battle between the big advertising platforms to be fierce, which will unlock opportunities at both ends of the spectrum (the very big/the very small).

Go big or go small, just don’t get caught in the middle. When it comes to advertising approaches, if you go small, community, ambassadors and advocacy are your friends. If you go big, we might see some reversion to tried and tested POS marketing tactics coupled with less pushes, but stronger. And if you dare try to scale from small to big, you better have some real organic power and some very effective boosters, because CAC will likely be a huge challenge.

And then what?

It’s likely this “Binary Paradigm” Age is the last age of Modern Advertising. After this, we’ll possibly be experiencing a tectonic shift. The combined efforts being put behind both web3 and the metaverse mean that the rules of the game will MASSIVELY change. The one big caveat though, is that we’re still far, far away from this being a mainstream reality given multiple hard technical challenges.

Until then, it’ll be interesting. For a while now we were stuck in a FB/Google advertising duopoly. This now seems up for grabs, and I for one welcome the competition it will generate.