By Santiago Hunt

2021 has forced the market (and me) to look away from the darling growth names and back to reality. As such, I’ve redoubled efforts at understanding the profitability puzzle, and Gross Margin is a big piece of it. It goes without saying that Gross Margin does not equal profitability. Nevertheless, it is a (if not “the”) fundamental building block behind solid unit economics.

However, GM% has limitations. While good at portraying the core unit economic logic of a product/service, it lacks information on how efficient a company is at achieving this GM%, nor how comparable it is to sector peers.

The following exercise tries to sidestep some of these issues. To normalize gross margin across peers, I’ve calculated gross profit x “operational atomic unit”. What does “operational atomic unit” mean? It’s the lowest common denominator for the operation of a business. Eg. In the case of social media, I’ve normalized GP (gross profit) x DAU (Daily Avg. Users). This allows for a comparable view, which offers better insight on the true picture behind social media’s cost structure & efficiency at a unit economic level.

Below you’ll find four different “operational atomic unit” comparisons:

1. Social Media: GP x DAUs (some exceptions based on MAU/QAU).

2. Paid/Freemium Platforms: GP x Paying User/Subscriber

3. Marketplaces: GP x User

4. SaaS: GP x Customer

And some bonus tracks…

Caveats

This exercise is fundamentally constrained by: i) being based on public data (tons of missing players but no good public info) ii) variability behind how different companies define the same metric iii) differences in time measurement (Eg. DAU vs MAU vs QAU) iii) the fact that no 2 businesses are alike. Therefore, there’s bound to be a lot of “apples vs. oranges”, as well as some inaccuracies given the need to simplify and standardize incongruous data. I suggest that you stop reading if you’re going to get caught up on this.

For standardization purposes, I’ve used LTM (Last Twelve Months) gross profit, but Q3 latest figures for “operational atomic units”. This has clear drawbacks, but it is the easiest way to guarantee comparisons are done on the same ground. And, as always, none of this financial advice. #DYOR.

1. Social Media

Social Media is an example of the limitations of GM%. See below:

Pure play social media platforms show somewhat similar degrees of GM%, accounting for differences due to type of ad inventory, engagement and higher/lower pricing power. Facebook leads, followed by Pinterest, and Twitter and Snap show the monetization difficulties they face vs peers.

I’ve included other options such as Garena, Roblox and Spotify. They’re not pure play social media, but are relevant given they compete for “user engagement”. Both Roblox and Spotify face clear GM% constraints. Their limited ad capabilities require direct user spend to fund them (limiting price power). Additionally, they face higher cost of goods: Spotify has a concentrated record label market on the supply side, while Roblox runs a much more fragmented product. ($SPOT and Garena are covered from a sub/paying user perspective later on).

Having said this, how much gross profit do these companies generate for each DAU (Daily Avg. User) they have?

First takeaway: Facebook is a beast. Yes, we already knew this given the amount of users they have. But the fact that they make 3-10x more GP per user than their competitors talks to how brutally efficient and powerful their advertising machinery is. Internet power laws are a thing, and Facebook is living proof (btw, the numbers don’t change much if you use MAUs instead of DAUs).

Second takeaway: If you’re only going to make 3-7 usd per user of GP, you’re going to need A LOT of users to make the flywheel work. 300-400M won’t be enough long term, and that’s the challenge Pinterest, Snap and Spotify face. You either go BIG, or you need to rethink your business model. This is particularly true for $PINS and $SNAP, which have taken a (related?) massive share price hit in 2021.

Third takeaway: If you can’t beat FB, don’t fight in the same turf. Twitter is a hated stock for many valid reasons. But it seems to have a viable, more focused monetization model. Furthermore, it’s likely that under new management this will be reinforced – the question being how far before breaking the platform.

Fourth takeaway: Games are hard. There’s no place where Internet power laws come more into play. As an example, take Candy Crush, where allegedly 0.4% of its users generate 50% of revenue. As such, it might seem unfair to look at GP x total users. But the truth is most games rely on becoming social phenomena to monetize at scale. Neither Roblox/Free Fire would be able to drive their heavy user spend without their massive player base. And these are two of the most successful franchises out there. Imagine how hard it is for the rest.

2. Paid/Freemium platforms

Next up are pay/freemium platforms. The common thread across these companies is: i) they compete for user attention (it’s hard to use two of these at the same time) ii) they offer some form of pay/subscription model. Keep in mind that all companies listed here have free usage available – except Netflix. Furthermore, some bolster their GP via advertising while others don’t (Match and Spotify doing so the most).

Despite massive variation between peers, these margins as a norm are clearly lower than social media. The ultimate payer here is a real life person and not a business, and that caps pricing power. What happens when looking at GP x Payer/Sub?

First takeaway: Is Match really that good? No, it’s not. Match is favored because a good part of its GP comes from advertising. Keep in mind that RPP (Revenue per payer) sits near ~15USD per quarter, and Match has struggled to increase it (except for APAC, Match’s hottest geography RPP wise).

Second takeaway: Global scale = lower GP x payer. Netflix and Spotify have the largest paying user base. This comes at a cost – they have the lowest GM%. And Netflix’s gp x sub would be the second lowest after Spotify’s if you consider number of viewers per HH (2.5 per HH?). Bottomline, global reach means catering to countries with lower disposable income, which means challenging economics.

Third takeaway: Spotify is in a tight spot. Low GM% + Low GP per subscriber = Trapped. Poor inherent profitability (low GM%) combined with low profit per user drives the need to acquire more users, which in turn means higher CAC long term.

You may know I’m not a fan of $SPOT (see “The ARPU Battle” for more). The fact that Spotify is now underperforming the 1Y/3Y S&P is quite telling (it vastly underperforms Nasdaq 3Y which is its fair benchmark). This doesn’t mean it’s a sell at these prices (it’s taken quite a hit). But it requires fundamental change to become a viable long-term investment (and podcasting hasn’t lived up to this yet).

3. Marketplaces

Be aware that this is the most disparate comparison set. Eg. Meli bundles eComm + Mercado Pago. Uber bundles Rides + Eats. Lyft measures quarterly, Uber monthly. Etc… Setting that aside, marketplaces allow for interesting analysis. Which would you say is the best business at first glance? Etsy, right?

Compare this with gross profit x user?

First takeaway: Etsy is two sides of the same coin. $ETSY is neither as good nor as bad as you might first think. It’s just a reflection of the nature of its business model. High unit economic profitability with lower repeat purchase. Whereas $MELI has a different model, value extraction that relies on the repeated flywheel usage of its ecosystem. Neither is good/bad, if managed. Ultimately though, businesses with low repeat purchase are inherently at risk (ETSY makes a point of improving shopping reliability – eg. “Star Sellers”).

Second takeaway: Uber/Lyft’s GM%s are misleading. Due to pandemic dynamics and driver disruption, both L12M GM% numbers are depressed. Critics will say (with good reason) they’re trapped between driver acquisition costs + rider subsidies. However, Uber in particular has pricing power combined with a high-fidelity customer base. GP x user points to this, and it may continue to improve during the next months. While $UBER bears have many good reasons to criticize it (spotty management track record), I’m long $UBER.

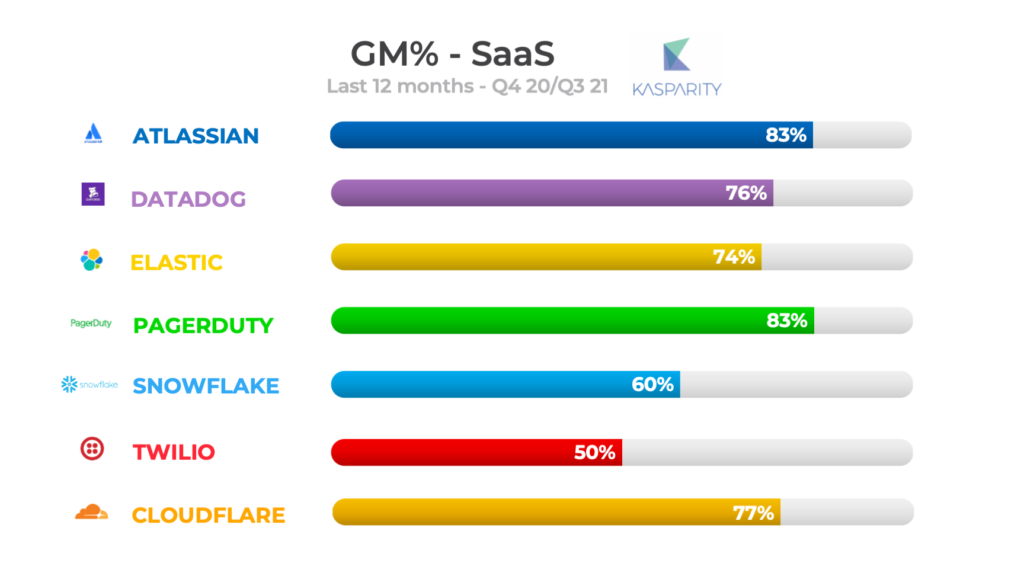

4. SaaS

SaaS is very different to all prior categories. B2B, few(er) customers, high GM% and high CAC coupled with longer sale cycles (Once again, insert “apples to oranges” disclaimer). “Mass SaaS” (Atlassian, Cloudflare and Twilio) have customers in the hundreds of thousands, whereas “Boutique SaaS” don’t go over 20K. Nevertheless, this is precisely what makes the comparison worth it.

Except for $SNOW and $TWLO, GM%s are similar across the board. This is not the case for GP x Customer.

First takeaway: Mass SaaS – the best of both worlds? Mass SaaS seems to combine high GM% + high customer scale. This has obvious advantages: As a norm, EBITDA for Mass SaaS is healthier than that of Boutique SaaS. The issue? As with network effects – the unwind can be devastating. Boutique SaaS have a series of moats which makes them hard to scale. But their product depth combined with sales & marketing barriers make them harder to breach. Mass SaaS low end GP x customer puts them at a riskier position in the SaaS world.

Second takeaway: In Boutique SaaS, NRR is key. “Net retention rate” (NRR) is likely the single most important metric to track for a SaaS business. Take DataDog, Elastic and PagerDuty. All have roughly similar customer count and GM% ($PD actually having a higher margin). What makes their GP x customer so vastly different? The fact that $DDOG’s NRR is 130%+, $ESTC’s is 125-130%, and $PD is ~120%. In simple terms: DataDog is vastly more efficient at extracting incremental dollars from their existing customer base than its peers…something you miss out when looking at GM% only.

Third takeaway: Snowflake is in a league of its own. A highly controversial company when it comes to valuation (at ~95B market cap, $SNOW is almost 100x P/S!). GP x Customer is one of the key reasons behind this valuation. $SNOW’s advocates will point to this as proof of how high value-adding Snowflake is, and that scalability will follow. But, even with this GP x customer, Snowflake bleeds money (-72% EBITDA L12M). It warrants a close look, but tread carefully here (Disclaimer: I have no position in $SNOW).

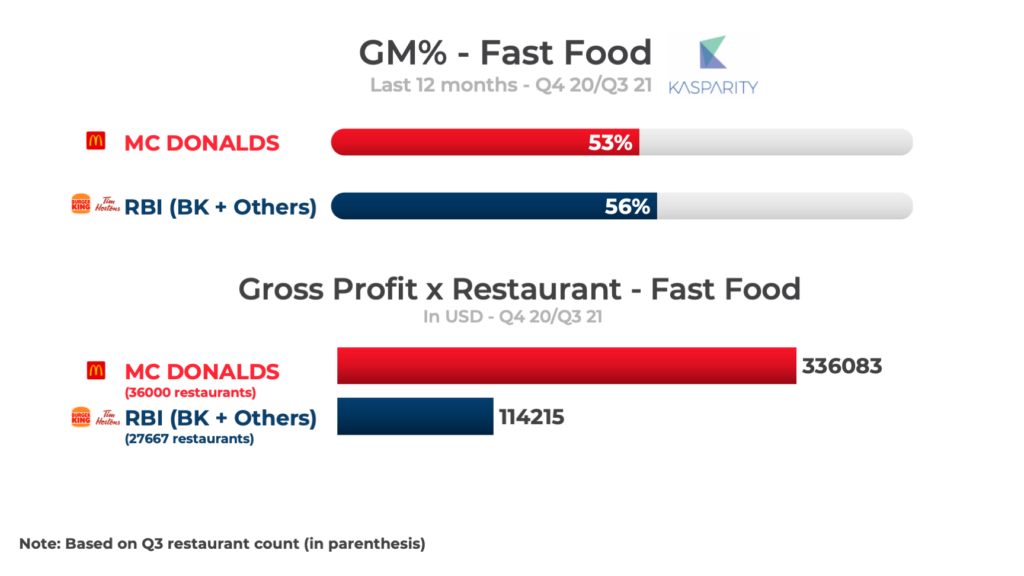

Bonus tracks

If I were a RBI shareholder I’d have a ton of questions (I’m not, look at 1Y/3Y/5Y returns of $QSR vs $MCD/S&P to see why).

This comparison ranges from pure play heavy engineering/mechanics all the way to digital transactions (which are ultimately 0s and 1s), with Tesla and Visa sitting at the two ends of this “real world vs digital world” spectrum. What’s most striking perhaps is that Sea’s GP x unit (excl. Garena) is lower than what Visa makes on a digital transaction… Bears will say “Told you so”, bulls will say “It’s a long game and there’s a path to profitability”. Personally, I think $SE’s management will have to get more vocal on the shape of this path moving forward.