By Santiago Hunt

ARPU (Average Revenue per User) has become one of the key go-to metrics tracked when assessing corporate performance. As with any isolated metric, it can lead to simplistic conclusions, particularly when comparing different ARPUs across different companies…

…So what better than to host the 2020 “ARPU Battle”? A direct ARPU comparison across top players in the “entertainment” business! Netflix, Spotify, Match (Tinder), Roblox and Garena (Free Fire). So much for my disclaimer on simplistic analysis 🙂

This comparison leads to a relevant discussion: Why did ARPU trajectories differ for these businesses in 2020? And what can help drive future ARPU for entertainment companies (or companies per se)?

It’s not apples to apples, or is it?

The obvious reader thought at this point: Are these companies comparable? What does Match have to do with Netflix? What does Spotify have to do with Roblox or Garena?

So before we get into the analysis, let’s run a quick review of what each business does:

Netflix: I’ll wager everybody is familiar with Netflix.

Spotify: Ditto Netflix. But just in case, Spotify is an audio on-demand global streaming platform.

Match: Parent company for most worldwide dating apps including Tinder.

Garena: The videogame developer/publisher arm of Sea Ltd ($SE). It is famous for Free Fire, the #1 grossing mobile game globally in 2019-2020.

Roblox: A 3D user generated ecosystem which has over 36 million users interacting and playing with it on a daily basis.

Video streaming. Audio streaming. Dating. Gaming. And a metaverse virtual game/world? Seems like too disparate a comparative set to extract any valuable conclusions.

And yet there is a common thread here. All of these companies are ultimately competing for people’s attention and leisure time. For the most part, R&R time spent in one of these platforms ultimately detracts from time spent in another one. Which makes comparing their ARPU trajectory an interesting exercise per se, and a very telling one when looking at 2020 and the pandemic dynamics.

ARPU in 2020

The Tl,Dr summary for this would be: For the most part, ARPU held stable for these companies when compared to 2019, with the notable exception of Roblox (UP!). But the devil is in the details. There’s an underlying thread about why Netflix has such a dominant position, and the potential for gaming (Roblox/Garena) to overtake this in the long run.

Netflix:

Netflix’s ARPU remained consistently stable throughout 2020 vs. 2019. Which makes sense given how established Netflix is a product, and how people know what to expect from Netflix. Two things stand out though:

i) Netflix’s ARPU is markedly higher than all these competitors. You could even divide it by 3 (~avg $NFLX household size?) and it would still be the highest of all.

ii) It managed to sustain this level of ARPU whilst delivering 24% Y/Y subs growth, attaining a base of over 200m subscribers (Q4 ’20). Impressive!

Of the 5 companies compared, Netflix is the only one with a “Pay 2 Access” model. Ie. You can’t use Netflix unless you subscribe, which differs from the “Freemium” models offered by the other platforms.

Spotify:

Spotify’s ARPU trajectory has been negative throughout 2020, averaging a 10% reduction vs. 2019 values. This is driven by a reduction in ARPS (Avg. Rev. per. Subscriber), which represents 87% of total Spotify revenue. A worrisome performance.

What makes this even more concerning is that this ARPU reduction hasn’t brought such a steep subscriber increase. $SPOT has shown a solid +27% subs growth, yet in line with a higher base like Netflix’s, and much lower than the fast-growing players in this comparative cohort. If you factor how $SPOT has way lower GM% vs. these competitors, questions about its business model become unavoidable.

Match:

Match has maintained a very stable ARPU in 2020, which is remarkable given the pandemic headwind for dating. Although I consider Match a player in this “entertainment cohort”, it’s fair to say that it’s the “odd-one-out” in many ways. Its revenue is driven by advertising, and its primary use case is more so being a dating enabler than an end destination for its users. Nevertheless, it’s massive global reach and user time spent make it an interesting contender.

Despite Match having an ad-based business model, increasing ARPU is vital if it is to be able to break free from the ad-revenue trap. Unless you’re Google, Facebook or a few other select names, being an ad-based business model is very limited by both your reach and your targeting capabilities. Subscribers and a strong ARPU are the path to avoid this trap, and as things normalize (hopefully) in a post pandemic world, it’ll be critical to see if Match can step up its ARPU and its mild subs growth trajectory, breaking its current plateau.

Garena (Free Fire):

Garena is the digital entertainment branch of Singapore based Sea Ltd, a company which currently has 3 main business units: the aforementioned Garena, Shopee (eCommerce) and SeaMoney (Digital Financial Services). Many people are not aware of the Free Fire phenomenon. Not only has it been the top grossing mobile game worldwide for the past 2 years, but it also has broken the 100M+ DAU mark at peak performance during 2020.

Garena’s ARPU had been consistently stable until H2 2020, where it showed a clear step up. The fact that this has been accompanied by a staggering 72% user growth y/y (Q4 ‘20) points to the fact that it’s likely a result of a planned move by the company in terms of steadily monetizing its very wide user base.

In this case, ARPU is reported as average booking per user. At 610M QAUs, this amounts to over 1B USD in bookings per quarter! It is worth noting that this is calculated across the whole universe of Garena players, where 88% play for free. If one were to calculate ARPU based on paying users only, it would be 15.48usd per quarter! A number by itself impressive, which becomes more amazing when taking into account Garena’s D+E footprint. What if even more QAUs could be converted to paying users…?

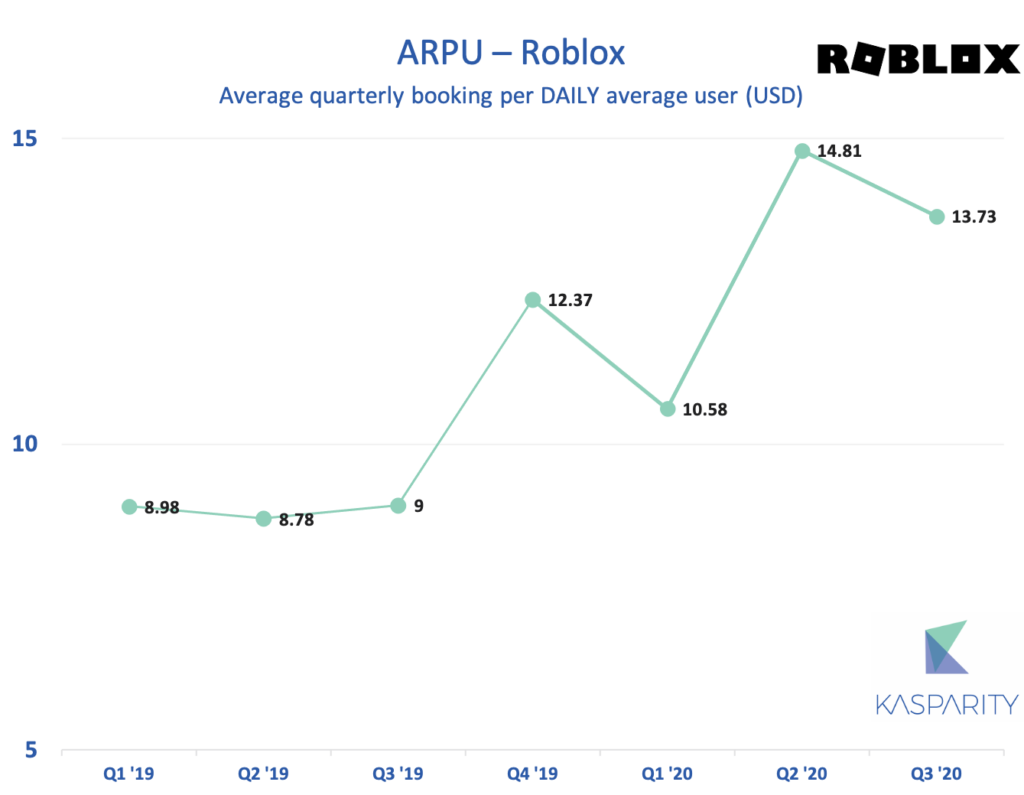

Roblox:

Last, but certainly not least, is Roblox.

Roblox’s numbers speak for themselves. Strong ARPU growth combined with unbelievable user growth (96% y/y). And keep in mind these numbers are missing Q4 2020 (unreported), which is a high seasonality period for $RBLX. Amazing!

Too good to be true? Part of this is driven by the fact Roblox chose to report ABPDAU (Average Bookings per Daily Avg. User) as an ARPU metric. Keyword here being “DAU” – a convenient way of propping up those numbers quite nicely. Nevertheless, while the absolute value might be murky, the trajectory is unquestionable.

One could argue Roblox has been benefited by the pandemic. This would be true, yet it would only scratch the surface. The fact is, it is likely that of the 5 companies in this cohort, Roblox embodies best some of the qualities required to sustainably drive ARPU long term.

What can make ARPU stronger?

4 things worth considering, in particular for proposals that aim at capturing “entertainment/leisure” time.

i) Immersion:

The deeper the immersion, the higher the ARPU potential. This is somewhat of a no-brainer. Arguably today, the Netflix experience is by far the most immersive. Yet videogames hold a potential trump card in the long run given they require greater interaction and focus. This is why AR/VR are a constant “buzzword”. Even though the technology hasn’t delivered (yet), it will remain an evergreen opportunity because the size of the prize behind it is massive.

ii) Enablers vs. Destinations

The ARPU implications behind being an entertainment enabler vs. an entertainment destination per se are very clear when taking a look at Match. For the most part, Tinder & co. are steppingstones towards something else – an IRL dating experience – thus capping their ARPU potential.

On the other end of the spectrum is where Netflix and especially Roblox sit. Netflix has flipped the traditional consumer journey: Your end goal is not watching VOD and therefore going to Netflix. Instead, your end goal is to browse Netflix for VOD. The distinction is subtle but important, and has been built upon Netflix’s customized feed + its original content.

Roblox is the ultimate destination example. It’s very hard to classify Roblox. It is not a game per se. It is not a social network per se. It’s a virtual world, which can mean many things or none at all. But one thing is clear: Users go to Roblox to…engage with other people & content in Roblox. The fact I had to use the word Roblox to define what Roblox is the ultimate litmus test of being a destination.

iii) Multisensorial stimuli

Multisensorial stimuli is a close sibling to immersion. Although not all immersive experiences are multisensorial, the greater the sensorial richness, the greater the immersion.

This is Spotify’s Achilles heel. Being audio only, the Spotify experience is limited by the limitations of audio. And although one could argue that one could use Spotify while multitasking thanks to being audio only, this in turn leads to Spotify being an enabler and less of an immersive experience.

What is most interesting here is not the present state of these platforms, but the future potential that multisensorial stimuli offers. This is the reason why Netflix is so keen on exploring Interactive options. It is also the reason why games such as those from Garena are symbiotic with Twitch/Booyah/YT/Discord. And it offers the potential for a massive unlock for Match with AR/VR!

Conversely, this creates a low ceiling for Spotify. The audio only focus lends to a clear and sharp positioning. But it comes at the price of capping long term ARPU potential.

iv) Digital profiles vs. Digital personas

This is where Garena and Roblox shine. Both have transcended the territory of offering their users “profiles” and are instead in the realm of digital personas (identity). Rebooting or churning away from these identities comes at a cost. Eg. In Free Fire’s case you’d lose virtual clout (badges, weapons, skins, emotes, etc.). But perhaps more importantly, you’d lose your virtual persona, your gateway to connecting with friends and peers. Something which is particularly painful if these platforms have become destinations per se.

Curiously, it’s likely that Netflix is the one in the weakest spot here. While the Netflix algorithm plays an important role in terms of content discovery, it is of secondary order when considering the Netflix deal a subscriber buys into. Furthermore, one could churn out of their Netflix profile, come back a few months later, and see no massive loss from a digital persona standpoint.

The implications down the road

To be fair, short term ARPU is a bigger of function of pricing & promotional strategies. There are a number of things that are overlooked here: competitive pressure, subsidizing users, buying penetration, geographical expansion…the list is a long one. But long term ARPU is where the game is ultimately won or lost. And that’s why keeping these points in mind is vital, because they have major implications that tie in deeply to UX/UI and the technology stacks upon which these companies are built.

Long term ARPU, coupled with penetration and churn, are the building blocks for revenue down the road. What are the implications of what we discussed here? Could we foresee a Netflix offering that aims at driving interactive and/or multisensorial formats? Can Match become a destination for the majority of its users, and not just a means to an end? Can Garena make Free Fire not just a game but a social network? Will Roblox further expand its monetization given its leading hand in terms of owning digital personas for Gen Z? And how can Spotify outmaneuver the tight spot it is sitting in?

One final note: while a fundamental consideration for long term investing, ARPU is still one piece of the bigger puzzles that all these businesses are. Therefore, don’t take any of this as financial advice. Please do your own research!